This article will show how underwater funds are handled in Fundriver on FAS 117-1 reports.

Please note that the FASB standards board replaced the FAS 117 reporting requirement with Accounting Standards Update 2016-14 beginning after December 15, 2017. This report complies with the old standard and should not be used for current accounting and audit purposes. Please use this report for periods prior to your organization’s adoption of ASU 2016-14.

The final report (Report 117-1 by fund - through 11-30) brings everything together. Here you can see the zeroing out of the components of unrestricted and the re-characterization to temporarily restricted. The totals net to the current year amounts.

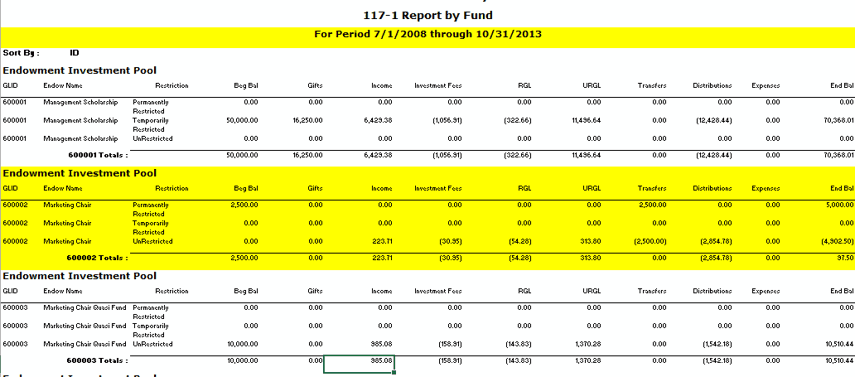

The first report (Report 117-1 by Fund - prior to transfer) includes a highlighted fund that is underwater and reflects the whole time period that the funds has been in existence. All the activity (that does not impact principal) and income allocations are classified as unrestricted.

The next report (Report 117-1 by Fund - July through Oct.) shows activity for the current year for this fund while it was still underwater. Please note that the first report (prior to transfer) includes current year data as well.

The final report (Report 117-1 by fund - through 11-30) brings everything together. Here you can see the zeroing out of the components of unrestricted and the re-characterization to temporarily restricted. The totals net to the current year amounts.

Ultimately, the driver for this breakdown is the historic gift value netted against the fund's total market value. You will note that this fund (just prior to the fund coming out from being underwater) had a permanently restricted balance of $5,000. However, the fund had a market value of $97.50. Thus, the unrestricted amount for the fund was $(4,902.50).